Last month saw 360 VC investments across Europe, with $8.2 billion invested in total – a 86% increase in funding volume compared to February.

Number and volume of announced funding rounds over the past 12 months*

- Number of funding rounds

- Invested volume in $bn

Leading Industries and Investors

According to the number of conducted investments, AI leads with 127 investments, followed by Health Care with 87 and FinTech with 72, each ahead by a significant margin of the next industry, Energy (42).

Kima Ventures was the most active investor in March with 8 announced investments. Followed by Bpifrance, Octopus Ventures, LocalGlobe and Daphni with 6 investments each rounding out the top five most active investors.

Top 10 Industries of Financed Startups

- AI

- Health Care

- FinTech

- Energy

- Manufacturing

- BioTech

- Food and Beverage

- Retail

- Web

- Marketing

Top 5 Investors with the highest number of deals

- Kima Ventures

- Bpifrance

- Octopus Ventures

- LocalGlobe

- Daphni

Notable funding rounds across Europe

In March, the largest funding round was a $2.0 billion Series C by Nscale, a London-based builder for AI data centers and provider for GPU cloud infrastructure that companies use to train, run, and scale large AI models. Founded in 2024 in the UK, Nscale raised the investment mainly to further accelerate their global development of vertically integrated AI infrastructure.

While Seed Rounds made up the largest share of rounds (43%), the highest investment volume was in Series C Rounds, which accounted for $2.66 billion across 8 deals.

The largest Seed Round was secured by Advanced Machine Intelligence, a Paris-based company which develops artificial intelligence systems that model real-world environments using sensor data. Founded in 2026 in France, AMI raised $1.03 billion (€892 million) in March.

Number and total volume of financing rounds per stage

- Number of funding rounds per stage

- Volume of financing rounds per stage in $mn

Detailed overview by stage

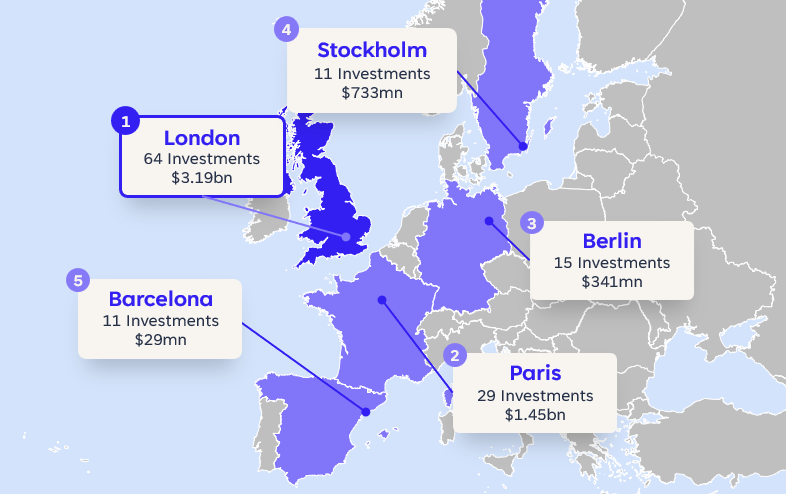

European VC Industry Hotspots

In March, London remained the leading hotspot for European VC by number of investments (64), followed by Paris (29), Berlin (15), Stockholm (11) and Barcelona (11).

The most investments by country were in the UK (96), followed by Germany (52) and France (44).

When ranked by investment volume rather than the number of investments, Lausanne ($237mn) with 4 investments joins London, Berlin, Stockholm and Paris in the top 5 cities.

VC Exit Overview

In March, 35 exits took place but contrary to last month, there was no IPO.

With 21 exits, FinTech companies were the largest exit industrie, followed by Health Care (7) and AI (7) companies.

Most companies exited in the United Kingdom with 15 exits, followed by 4 companies in France.

- Number of Acquisition Exits

- Number of IPO Exits

PE Acquisitions Overview

In March, 41 PE acquisitions (10% of all VC and PE investment rounds) were conducted, an increase of 2pp compared to last month.

With 10 acquisitions, the UK saw the highest number of companies acquired in February.

Manufacturing (9), FinTech (9), ProTech (7), Health Care (6) and Scurity (3) were the top acquisition industries mentioned.

The standout deal was Brookfield’s €~1.2 billion acquisition of Fidere, a real estate company which focuses on acquisition& management of residential properties for rent.

- % of all investment rounds

- Number of PE acquisitions

*All data from CrunchBase, as of April 2, 2026.

Partner with us

Unlock the full potential of your financial strategy with Trustventure’s expert guidance. Whether you’re navigating challenges in the financial sector, seeking advice on corporate financing, or enhancing your planning and controlling processes, we’re here to empower your journey and help you create transparency and confidence for you and your investors.

Ready to elevate your financial game? Reach out to us today using our contact form or drop us a direct message at office@trustventure.de. Work with us to achieve your financial success! 🚀

Other articles

VC Landscape Germany Venture Capital Landscape – Q2 2026

Between an increase of 5% in invested VC volume and a €600mn funding round in the DefenseTech space, Germany is closing its venture capital landscape Q2 2026. Learn all about it in our latest analysis.

July 22, 2026

VC Landscape Germany Venture Capital Landscape – Q2 2026

Between an increase of 5% in invested VC volume and a €600mn funding round in the DefenseTech space, Germany is closing its venture capital landscape Q2 2026. Learn all about it in our latest analysis.

July 22, 2026

VC Landscape European Venture Capital Landscape – June 2026

With 420 investments and $7.5 billion raised across Europe, June saw a 18% increase in volume and 43% rise in deal count month over month. The largest round of the month was a $1.4 billion Series C by the Metzingen-based company Neura a company which builds AI-powered cognitive robots for industrial and everyday use.

July 21, 2026

VC Landscape European Venture Capital Landscape – June 2026

With 420 investments and $7.5 billion raised across Europe, June saw a 18% increase in volume and 43% rise in deal count month over month. The largest round of the month was a $1.4 billion Series C by the Metzingen-based company Neura a company which builds AI-powered cognitive robots for industrial and everyday use.

July 21, 2026

M&A European Roll-Up Market Report – June 2026

June 2026 presented a 3% year-over-year decrease in the number of PE-backed acquisitions. In addition to Software, private equity investors are also targeting FinTech, Health Care and Consulting. Learn all about it in our report and case study, including Blend360’s acquisition of In516ht.

July 8, 2026

M&A European Roll-Up Market Report – June 2026

June 2026 presented a 3% year-over-year decrease in the number of PE-backed acquisitions. In addition to Software, private equity investors are also targeting FinTech, Health Care and Consulting. Learn all about it in our report and case study, including Blend360’s acquisition of In516ht.

July 8, 2026

M&A European Roll-Up Market Report – May 2026

May 2026 presented a 45% year-over-year increase in the number of PE-backed acquisitions. In addition to Marketing, private equity investors are also targeting Software, FinTech and Consulting. Learn all about it in our report and case study, including RSK’s acquisition of HV Energy Systems.

June 15, 2026

M&A European Roll-Up Market Report – May 2026

May 2026 presented a 45% year-over-year increase in the number of PE-backed acquisitions. In addition to Marketing, private equity investors are also targeting Software, FinTech and Consulting. Learn all about it in our report and case study, including RSK’s acquisition of HV Energy Systems.

June 15, 2026

VC Landscape European Venture Capital Landscape – May 2026

With 293 investments and $6.3 billion raised across Europe, May saw a 31% increase in volume and 10% decrease in deal count month over month. The largest round of the month was a $2.1 billion Series B by the London-based company Isomorphic Labs an AI-first drug design and develoment company that transforms drug discovery to design and evaluate new medicines.

June 8, 2026

VC Landscape European Venture Capital Landscape – May 2026

With 293 investments and $6.3 billion raised across Europe, May saw a 31% increase in volume and 10% decrease in deal count month over month. The largest round of the month was a $2.1 billion Series B by the London-based company Isomorphic Labs an AI-first drug design and develoment company that transforms drug discovery to design and evaluate new medicines.

June 8, 2026

VC Landscape Germany Venture Capital Landscape – Q1 2026

Between an increase of 6.5% in invested VC volume and a €350mn funding round in the AI space, Germany is closing its venture capital landscape Q1 2026. Learn all about it in our latest analysis.

May 20, 2026

VC Landscape Germany Venture Capital Landscape – Q1 2026

Between an increase of 6.5% in invested VC volume and a €350mn funding round in the AI space, Germany is closing its venture capital landscape Q1 2026. Learn all about it in our latest analysis.

May 20, 2026

VC Landscape European Venture Capital Landscape – April 2026

With 327 investments and $4.8 billion raised across Europe, April saw a 42% decrease in volume and 9% fall in deal count month over month. The largest round of the month was a $1.1 billion Seed Round by the London-based company Ineffable Intelligence, which develops machine learning systems that learn through interaction and experience.

May 13, 2026

VC Landscape European Venture Capital Landscape – April 2026

With 327 investments and $4.8 billion raised across Europe, April saw a 42% decrease in volume and 9% fall in deal count month over month. The largest round of the month was a $1.1 billion Seed Round by the London-based company Ineffable Intelligence, which develops machine learning systems that learn through interaction and experience.

May 13, 2026

M&A European Roll-Up Market Report – April 2026

April 2026 presented a 0% year-over-year increase in the number of PE-backed acquisitions. In addition to Consulting, private equity investors are also targeting Software, FinTech and Transportation. Learn all about it in our report and case study, including NOD’s acquisition of Paintworks.

May 11, 2026

M&A European Roll-Up Market Report – April 2026

April 2026 presented a 0% year-over-year increase in the number of PE-backed acquisitions. In addition to Consulting, private equity investors are also targeting Software, FinTech and Transportation. Learn all about it in our report and case study, including NOD’s acquisition of Paintworks.

May 11, 2026

M&A European Roll-Up Market Report – March 2026

March 2026 presented a 19% year-over-year increase in the number of PE-backed acquisitions. In addition to FinTech, private equity investors are also targeting Consulting, Software and Marketing. Learn all about it in our report and case study, including Syndigo’s acquisition of Taggstar.

April 16, 2026

M&A European Roll-Up Market Report – March 2026

March 2026 presented a 19% year-over-year increase in the number of PE-backed acquisitions. In addition to FinTech, private equity investors are also targeting Consulting, Software and Marketing. Learn all about it in our report and case study, including Syndigo’s acquisition of Taggstar.

April 16, 2026